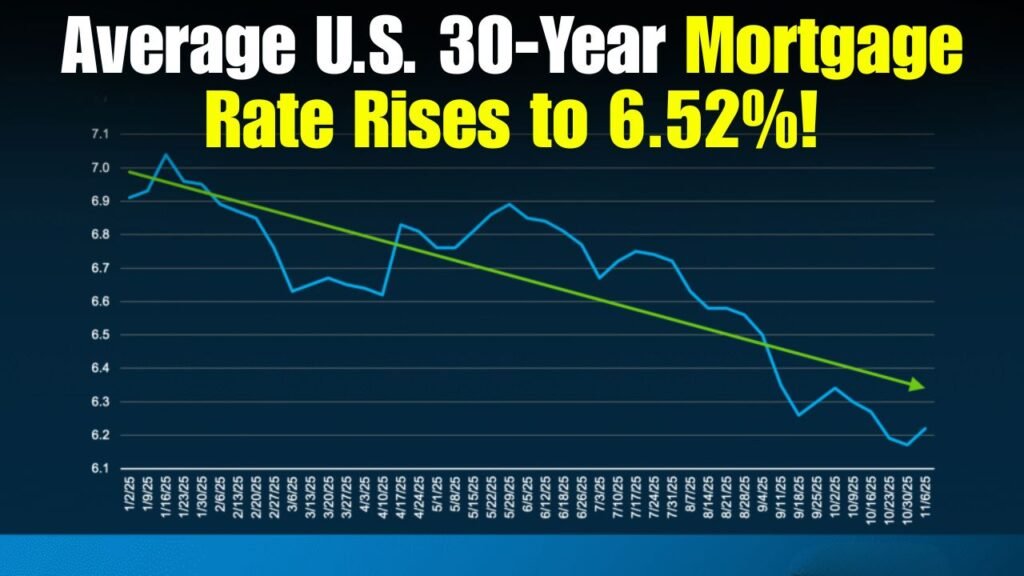

Average US 30 year mortgage rate rises to 6.52 percent in housing market update

Average US 30 year mortgage rate rises : The US home market is once again under pressure with the average 30-year fixed mortgage rate rising to 6.52 percent in the latest market update. The hike comes as purchasers already face high house prices, a tight housing supply and continued uncertainty about the trajectory of interest rates. Mortgage rates continue to be one of the largest factors affecting affordability, and modest changes can make a big difference in monthly payments for purchasers across the country. As the housing sector continues to transition to a higher-rate environment, financial markets, lenders and housing experts are intently watching these events.

Mortgage rates at 6.52 percent for 30-year loans

The 30-year mortgage rate, the most popular home loan product in the U.S., is up to an average of 6.52 percent. That increase is consistent with broader economic trends, including inflation expectations, signals from the Federal Reserve on its policy moves and changes in Treasury bond yields. Higher borrowing costs translate into higher monthly mortgage payments for prospective homebuyers, making affordability an increasing worry. Rates are still much higher than the ultra-low levels recorded during the pandemic period, albeit they remain below some of the peaks seen in recent years.

Homebuyers struggle with higher borrowing costs

The recent rise in mortgage rates is yet one more barrier to entry for purchasers hoping to get a foothold in the home market. A higher interest rate implies borrowers pay more money over the life of a loan even when purchasing the same home. This has meant that some potential purchasers are delaying purchases, cutting budgets or exploring other financing. Affordability is a key challenge for first-time homebuyers. Rising mortgage rates and sky-high property prices have eroded purchasing power across much of the country. Buyers who were qualified for larger loans a few years ago may be looking at less expensive homes now.

Impacts on housing market activity

Higher mortgage rates are projected to dampen activity in the housing market overall. And higher borrowing costs usually cool demand, as purchasers grow cautious. That can mean fewer house sales and longer time on the market for properties in some markets. However, the housing market has proved resilient despite rate swings. High levels of employment and ongoing demand for home ownership have underpinned activity in many places. Some markets may see reduced sales, while others will remain competitive due to tight housing inventory.

Sources : Alzehimer’s Association

Fed policy remains a key factor

Mortgage rates don’t directly move up and down with decisions made by the Federal Reserve, but the central bank’s decisions have a major influence on the cost of borrowing. Investors are keeping a tight eye on inflation statistics and economic signs for hints of future interest rate changes. If inflation stays stubborn, market players may expect interest rates to stay higher for longer. On the flip side, signals of falling inflation could set the stage for cheaper borrowing costs down the line. These assumptions tend to influence mortgage rates far before the formal policy change.

Housing Supply Continues to Drive Prices

Many locations of the United States are still seeing very tight home inventories even with increasing mortgage rates. Homeowners who got cheaper mortgage rates in earlier years may be hesitant to sell and take on more expensive financing on a new property. This has led to a shortage of suitable homes in a number of markets. Tight supplies have buoyed home prices even as borrowing costs have climbed. While there have been certain local markets that have witnessed price corrections, house values across the country have been more steady overall than many observers initially anticipated.

What a Mortgage Rate Increase Means for Homeowners

Most existing homeowners with fixed-rate mortgages are mostly shielded from the recent hike. Their monthly mortgage payments stay the same until they want to refinance, move, or borrow against the property. However, increased rates could limit the financial benefits for homeowners looking to refinance that were available when rates were lower. Many borrowers are opting to stay with their present mortgages instead of refinancing at today’s rates.

Outlook for the Next Few Months

Housing specialists say mortgage rates are expected to remain sensitive to economic data, inflation trends and movements in financial markets. The projections are mixed, but analysts agree that borrowing prices will remain volatile, not snap back quickly to the lows of the past. Potential buyers and sellers will likely continue to adjust to the higher-rate climate. Market activity may hinge on how soon inflation eases and whether economic conditions would allow for more interest rate cuts. Until then, affordability will continue to be a major concern for many households looking to buy a home.