Delaying Social Security Can Cost Retirees Thousands More Than They Expect

Delaying Social Security Can Cost Retirees Thousands Delaying Social Security Could Cost Retirees Thousands More Than They Expect This is often a surprise to retirees because many believe that waiting longer always guarantees a better financial outcome. In reality, the age to claim benefits will depend on your personal situation, life expectancy, health, income needs and retirement savings. Delaying Social Security past full retirement age can result in permanent increases in monthly benefits due to delayed retirement credits, but waiting too long without a clear plan or waiting past age 70 can actually reduce lifetime income. Retirees can avoid costly mistakes and maximise their retirement security by knowing the system before applying for benefits.

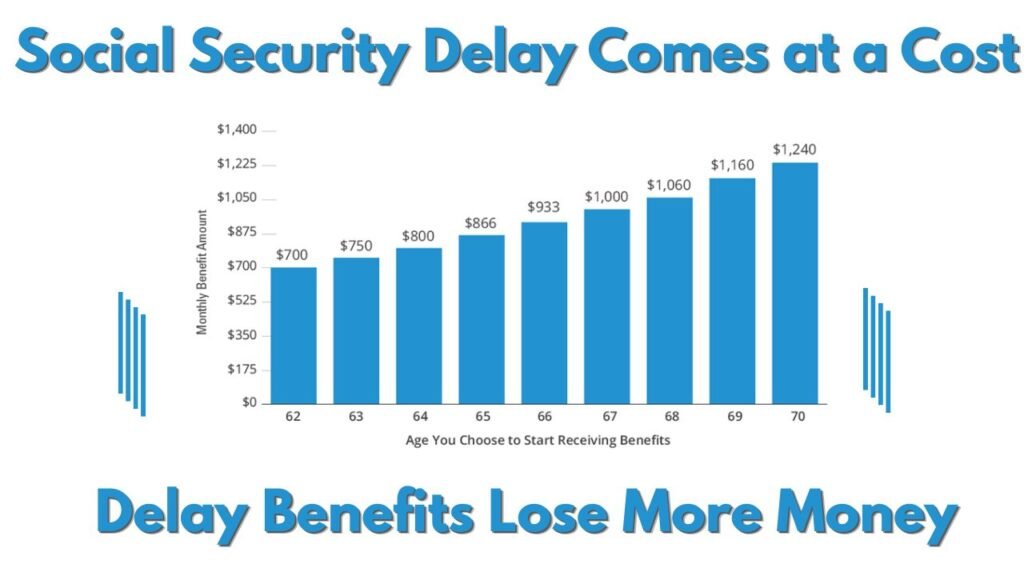

Many financial experts say retirees should compare lifetime expected benefits, not just the size of the monthly checks. For those born in 1943 or later, delayed retirement credits typically boost retirement benefits by about 8 percent for each year after full retirement age until age 70. But those additional monthly payments provide value only if the retiree lives long enough to reach the break-even point, which is typically around age 80 based on individual circumstances. That is why all retirement decisions should be made based on individual financial planning and not generic advice.

Latest Update on Delaying Social Security Benefits

The Social Security Administration still allows retirement benefits to start as early as age 62, and as of 2026, delayed retirement credits will no longer be granted at age 70. There’s no monetary advantage to waiting past age 70, when monthly benefits cease to grow. Therefore this decision should be taken prior to this milestone.

Official Social Security Website and Benefit Information

The Social Security Administration (SSA) is the official source for information on retirement benefits. Retirees can sign into their personal Social Security account to get an estimate of future monthly benefits, compare ages for claiming benefits, see a history of their earnings and apply for retirement benefits online.

- Agency: Social Security Administration (SSA)

- Benefit calculators are available through your personal SSA account.

- Eligible applicants can apply for retirement online .

- Your earnings record and benefit estimates

How Delaying Social Security Benefits Can Affect Retirement Income

If you wait until you reach your full retirement age, you get a higher monthly retirement benefit because of what are called delayed retirement credits. If you were born in 1960 or later, your full retirement age is 67. If you wait to take benefits until you are 70, you will get about 24% more per month than if you had claimed at your full retirement age. Yet the delay also means years of payments lost.

The money trade-off is huge. Those who cash in early get more checks in their lifetime, but those who wait get less, larger checks. Retirees in poorer health or with less time left to live may reap more lifetime benefits by taking benefits earlier. On the other hand, healthy retirees who plan to enjoy the benefits of a long retirement by waiting until 70.

Important Documents and Retirement Planning Instructions for Social Security

All retirees should collect all the necessary information before applying for retirement benefits to make sure that it is processed properly.

- Social Security No.

- Proof of age/birth certificate

- Work experience

- Any recent tax records

- Bank account information for direct deposit

- marriage or divorce records, where applicable,

- Check the earnings history for errors before you possibly file

It is also important to sign up for Medicare when you are eligible. While you can delay Social Security without delaying Medicare, if you miss Medicare deadlines, you can face lifetime penalties to your premiums.

Smart Retirement Advice Before Delaying Social Security

One of the biggest retirement decisions most Americans will face is when to take Social Security. The bigger monthly check sounds good, but waiting to collect benefits isn’t always the best decision for everyone. For those with substantial retirement savings and good health, waiting until age 70 can be beneficial. But those who need immediate income or who have medical concerns may get more lifetime value by claiming earlier.

Experts usually advise you to review your retirement savings, your life expectancy, taxes, spousal benefits and overall financial goals before you make your final decision. Retirement planning is not one size fits all, and personalised planning often results in better outcomes than generic recommendations.